Western Electronics (In-depth) Giantec Semiconductor: DDR5 SPD Sees Volume Growth, Automotive EEPROM Expands New Horizons

Special Notice: The "Measures for the Appropriate Management of Securities and Futures Investors" and the "Guidelines for the Implementation of Appropriate Investor Management by Securities Business Institutions (Trial)" officially came into effect on July 1, 2017. The push information produced through new media formats on this official account is intended solely for professional investors of Western Securities. If you are not a professional investor of Western Securities, please unsubscribe from this account and cease subscribing to, receiving, or using any push information from it. Due to access restrictions on this official account, we apologize for any inconvenience caused. Thank you for your understanding and cooperation.

Special Statement: The "Measures for the Administration of Appropriate Suitability for Securities and Futures Investors" and the "Guidelines for the Implementation of Appropriate Suitability Management by Securities Business Institutions (Trial)" officially came into effect on July 1, 2017. The push notifications produced via new media formats on this official account are exclusively intended for professional investors of Western Securities. If you are not a professional investor of Western Securities, please unfollow this official account and cease subscribing to, receiving, or using any push notifications from it. Due to access restrictions on this official account, we apologize for any inconvenience caused and appreciate your understanding and cooperation.

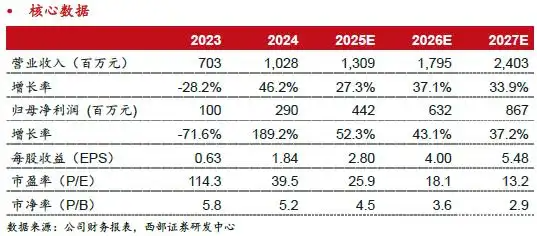

Key Takeaways: We forecast that Giantec Semiconductor's revenue for 2025/2026/2027 will be RMB 1.309/1.795/2.403 billion, with net profit attributable to shareholders of RMB 442/632/867 million. Using the comparable company valuation method, we assign Giantec Semiconductor a 27x P/E ratio for 2026, corresponding to a target market cap of RMB 17.073 billion and a target price of RMB 107.98. This is our first coverage, with a "Buy" rating.

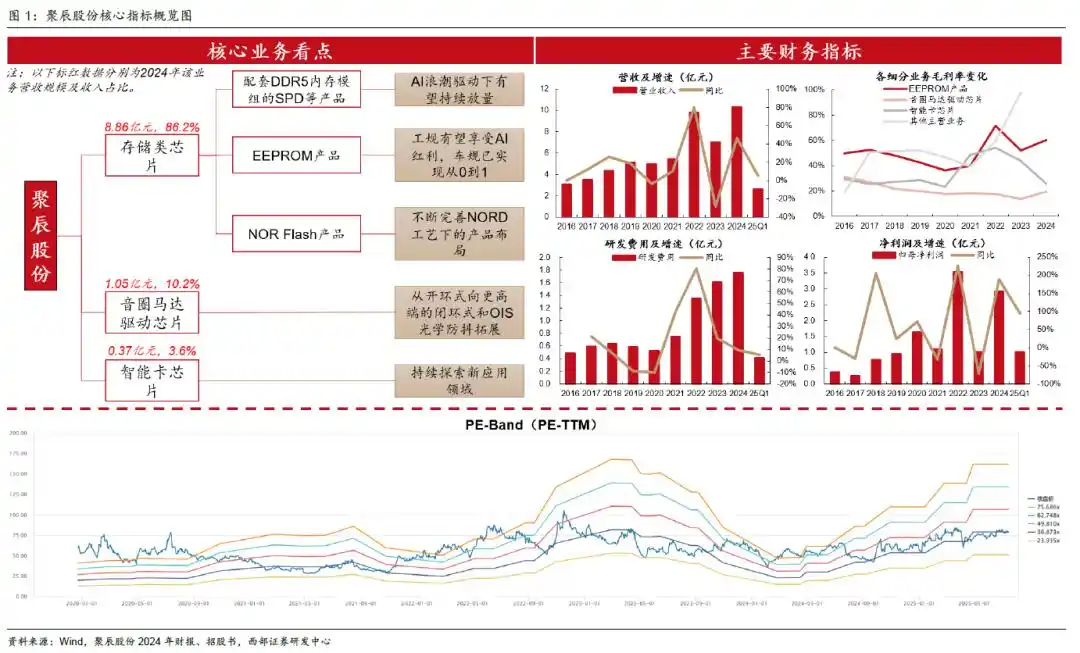

Global Leader in EEPROM. Giantec Semiconductor originated from ISSI and has decades of experience in EEPROM R&D. As early as 2012, it became a supplier of EEPROM for Samsung smartphone cameras, benefiting from the smartphone upgrade cycle from 2013 to 2021. Since 2022, the company has successfully entered the supply chain for server and PC memory modules through its DDR5 SPD chips developed in collaboration with Montage Technology, marking its second growth phase. In 2024, its automotive-grade EEPROM products began ramping up, poised to become a new revenue driver.

DDR5 SPD: Continued Penetration in Servers, Larger Potential in PCs. The company has been developing and selling SPD products for DRAM memory modules since the DDR2 era, with its latest DDR5 products now in volume production. Currently, DDR5 penetration in PCs lags behind servers. We estimate that when combined DDR5 penetration in servers and PCs reaches 85%, demand for SPD could peak at nearly 500 million units, indicating significant growth potential for the company's SPD business.

Industrial EEPROM Sustains Growth; Automotive EEPROM Achieves Breakthrough. Giantec has maintained its global leadership in smartphone camera EEPROM since 2018, with a peak market share of 42.7%. Although growth slowed in recent years, it is expected to rebound driven by AI smartphone upgrades and wearable demand. The company is one of the few global suppliers to enter the automotive EEPROM market, with this segment accounting for nearly 10% of total revenue in 2024. Rising localization demands from domestic automakers could accelerate its growth.

Exploring New Applications to Expand Boundaries. In NOR Flash, the company continues to refine its NORD process products, offering smaller sizes and lower costs than competitors, and is expanding into high-end applications like automotive. For voice coil motor driver chips, it is upgrading from open-loop to closed-loop and OIS stabilization solutions, with small-volume shipments to select customers already underway, expected to contribute to future earnings.

Key Assumptions

Memory Chips: The company’s memory chip business includes SPD, EEPROM, and NOR Flash.

1) SPD: Current growth is driven by server DDR5 memory module demand, with PC DDR5 modules also ramping up. DDR5 penetration is projected to rise from ~50% at the start of the year to over 70% by year-end. Factoring in market share gains and customer inventory/testing needs, we assume 47% SPD revenue growth in 2025, slowing in 2026/2027.

2) EEPROM: Historically focused on smartphones, growth stalled recently due to weak demand. Automotive EEPROM began scaling in 2024 but remains a small share; we project 50%/100% growth in 2025/2026, easing to 67% in 2027.

3) NOR Flash: Revenue is modest but expanding into automotive/industrial markets. We assume steady growth.

Overall, memory chip revenue is forecast at RMB 1.125/1.530/2.019 billion for 2025/2026/2027 (+27%/36%/32%). Gross margins are stable, but automotive EEPROM’s higher margins may lift the segment to 64.9%/66.3%/67.1%.

Voice Coil Motor Driver Chips: Current open-loop products have lower value/margins. Closed-loop and OIS solutions, now in small-volume production, should drive 40%/50%/50% revenue growth to RMB 147/221/331 million, with margins rising to 25%/30%/30%.

Smart Card Chips: A minor segment (e.g., access cards), with stable growth (0%/20%/20%) and margins (26%).

Differentiation from Market Views

DDR5 SPD: The market sees limited growth post-70% server penetration. We emphasize untapped PC potential and broader DDR5 adoption.